Northern Europe

“Overall, our Northern European business performed well in 2024 in a difficult market. Our multi-beverage platforms and strong market positions provide stability and a solid foundation, allowing us to maneuver safely through current market headwinds. In Norway, the integration of acquired entities, Hansa Borg & Solera, has been completed with the SAP implementation in January 2025”

Kalle Järvinen,

SVP Baltic Sea, Sweden & Norway and Managing Director Hartwall, Finland

Financial performance

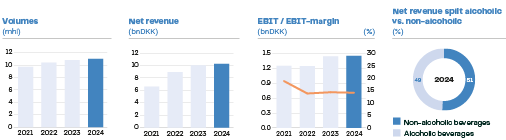

Total volumes increased organically by 2% in 2024 to 11.0m hectoliters, while net revenue increased by 3% to DKK 10,274m in 2024, however reflecting varying performance and market trends on country level, with flat developments in Finland and Norway, while Denmark, Sweden, and the Baltic countries displayed solid growth.

Development and initiatives in 2024

Denmark

Although the macro-economic situation in Denmark is better than in the rest of the Nordics, the beverage sector continue to be impacted by cautious consumer behavior as consumers are going out less and buying more on promotion.

Nevertheless, 2024 was a volume record year for Royal Unibrew in Denmark, which is a result of investments in our strong brand portfolio, our highly engaged staff, and outstanding in-market execution.

We are gaining market share in the majority of our portfolio, notably driven by CSD, energy drinks and drinks with enhancements.

In April, we launched our new isotonic sports drink, Faxe Kondi Pro with three different flavours, which has brought us close to a market leader position in the enhanced category, which is one of our growth categories.

Two years ago, we launched the Faxe Kondi Orange variant, which has been very well received, enabling us to battle for market leadership in the CSD orange category as well.

We also launched a new design for our energy drink, Booster, and gained significant market shares.

PepsiMax is the bestselling CSD brand in Denmark, and we have successfully implemented the design upgrade through a combination of extensive marketing campaigns, events, and in-store visibility.

In 2024, we rejuvenated our Royal Beer and launched two new beers, Royal Blanche and Royal IPA. Royal Pilsner 0.0% was voted as the best non-alcoholic beer in Denmark in 2024.

Our strong customer focus and local engagement were recognized by both the retail segment and On-Trade channel in 2024.

We were top-rated as the preferred partner in the retail segment, and our NPS score improved to “Excellent” in On-Trade.

The stellar performance across channels and categories is attributable to our highly engaged people throughout the value chain.

Norway

In Norway, we are predominantly catering to the alcoholic beverage segment, such as RTD/cider, beer, wine and spirits.

Like in the rest of the Nordics, cautious consumer behavior has had a significant negative impact on the On-Trade segment and caused consumers to trade down and look for cheaper alternatives, including higher appetite for tax-free and cross-border shopping.

While the consumption of beer, wine and spirits is declining, RTD/cider is increasing. It is primarily the low-calorie category, Hard Seltzer that is driving the growth, and we are part of driving the growth through new innovations and product launches.

In the Spring 2024, we launched Hansa Hard Seltzer Apple, complementing the Mango variant launched in 2023. The Apple variant was meant to be a summer launch only, but due to the product’s high popularity, it has now been included in the regular assortment.

Additionally, we have also launched Grevens Hard seltzer, using the brand’s strong position in Cider to introduce new products in an adjacent growing category.

In RTD, our partner brand Smirnoff Ice has taken considerable market share as a result of strong execution and in-store visibility.

Within wine and spirits, we have won our fair share of tenders from Vinmonopolet, and in general we have intensified our cooperation with strategic partners.

We also work with strong partner brands in CSD, notably Fever Tree and San Pellegrino. In both cases, we are growing sales and taking market share.

The integration of Hansa Borg & Solera has been completed, as we went live on Royal Unibrew’s SAP ERP-platform on January 6, 2025, which will ensure better decision making throughout the Norwegian business.

Finland

The Finnish market is still negatively impacted by low consumer confidence due to geopolitical uncertainty, higher unemployment rate, inflation and interest rates, although several economic indicators have started to move in the right direction. Consequently, Finnish consumers are saving more and spending cautiously, which is significantly challenging the On-Trade business and increasing the promotional pressure in Off-Trade.

Despite the challenging market environment, we have been able to protect revenue and improve profitability through price/mix focus.

In 2024, we successfully launched a number of novelties including Jaffa Lemonade, Novelle Plus and Original Long Drink Lemonade, all of which hit consumer trends and preferences well in all channels. Thus, the Long Drink hype seen in connection with the successful launch of Original Long Drink Pineapple in 2023, is continuing and boosting both the overall growth and our market share in the RTD category.

In 2024, Hartwall became the leading wine importer in Finland with the take-over of a distribution agreement of wines from Chile and Argentina.

In October 2024, an agreement was signed to acquire Richard Pernod’s entire portfolio of local brands with their related production facility in Turku. The brand portfolio includes Minttu peppermint liqueur, which is an iconic brand and must-have stock in Finland. The agreement is expected to be closed by February 28, 2025.

Baltic countries

Similar to Finland, the Baltic countries are impacted by geopolitical uncertainty, high inflation and lower consumer purchasing power. However, the On-Trade channel has not been hit as hard.

In general, consumers are looking for good brands, high value and good bargains.

In 2024, we continued our multi-beverage strategy implementation and gained market share in all our strategic focus areas: premium beer, CSD, RTD and energy drinks.

The main growth in 2024 was delivered by our local premium beer brands, Bauskas, Madonas, Vilkmerges and Kalnapilis, through new product launches, execution excellence and limited-edition craft beer.

Energy drinks maintained double digit growth in the Baltics in 2024, and we step-changed the sale of CULT and delivered significant market share growth owing to a successful innovation strategy, targeted brand building activities as well as high focus on execution excellence. The CULT brand expanded the energy drinks category by launching a zero-caffein product line.

The PepsiCo brand portfolio was among the fastest growing brands in the Baltic CSD market. We were both able to increase the market share considerably and to contribute to a positive category development. The developments were driven by continued increase of cold space, multiple touchpoints in retail, expansion of the On-Trade client base, and increased investments in brand building activities. We have been especially focused on the no sugar segment and Pepsi Zero, which was the fastest growing brand in the cola-flavor no sugar segment in 2024.